InspireMD (NSPR) and the quiet revolution in carotid artery stenting

InspireMD (NSPR) is currently trading at 1.65. That’s 45% down from its high. While Wall Street is busy looking elsewhere, this small company just launched what might be the best carotid stent ever made. Why is the market ignoring this?

That’s the disconnect I want to explore.

While the stock has been quietly ignored by most retail investors and under-covered by Wall Street, the company has spent the last several years building what may be the most clinically superior carotid stent in existence. It just received FDA approval.

⚠️ Reader notice: The author holds a position or has active interest in NSPR at the time of writing. Nothing in this article constitutes financial advice. All analysis is based on publicly available information. Do your own due diligence.

It just launched commercially in the United States. And it just reported its first full quarters of US revenue with sequential growth that would make most medtech companies envious.

The market’s response? The stock went down. Does that make sense? In my view, it’s a classic case of the price not reflecting the clinical reality. Yet.

What InspireMD Actually Does

Every year, hundreds of thousands of Americans are diagnosed with significant carotid artery stenosis, a dangerous narrowing of the arteries that supply blood to the brain. Left untreated or poorly treated, it’s one of the leading causes of ischemic stroke.

The traditional solution has been carotid endarterectomy, a surgical procedure where a vascular surgeon physically opens the neck, clamps the artery, and removes the plaque buildup. It works. It’s been the standard of care for decades. But it’s invasive, requires general anesthesia, carries real surgical risks, and isn’t suitable for every patient.

The alternative, carotid artery stenting (CAS), is less invasive. A catheter is guided through the femoral artery in the groin up to the carotid, and a stent is deployed to hold the artery open. No neck incision. Shorter recovery. Lower surgical risk profile.

The problem with traditional carotid stents has always been embolic risk, tiny particles of plaque dislodged during the procedure that travel to the brain and cause the very stroke you’re trying to prevent. First-generation stents were good at keeping arteries open. They were not great at preventing those particles from escaping.

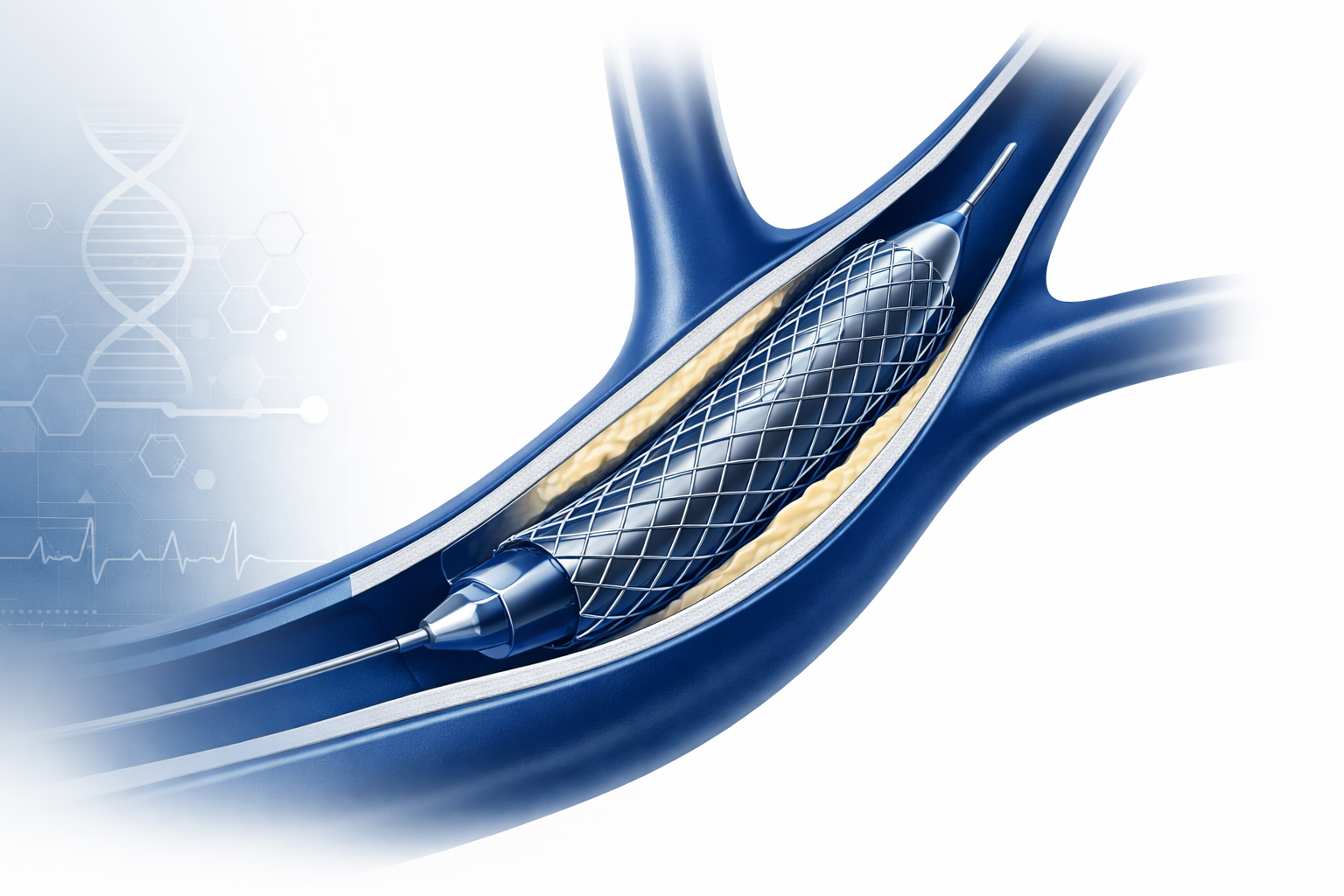

That’s the problem InspireMD’s CGuard Prime was designed to solve.

The Technology: Why MicroNet Changes Everything

CGuard Prime is built around a proprietary technology called MicroNet, a fine polymer mesh that wraps the exterior of the stent. Think of it as a biological net: it keeps the stent structurally sound while physically trapping embolic material before it can travel upstream to the brain.

The concept is elegant. The clinical results are extraordinary.

In the C-GUARDIANS pivotal trial — the study that secured FDA PMA approval in June 2025 — CGuard Prime demonstrated the lowest rates of major adverse events at both 30 days and one year of any carotid stenting pivotal trial ever conducted. The manuscript was subsequently published in the Journal of the American College of Cardiology in January 2026, peer-reviewed validation of the highest order.

The takeaway is simple: this isn’t just a ‘better’ product; it’s a peer-reviewed leader.

Over 70,000 CGuard implants have been performed globally across Europe, the Middle East, Asia-Pacific, and Latin America. The real-world track record exists. The safety profile is established. This is not a speculative technology, it’s a proven one that just entered the largest medical device market in the world.

The Market Opportunity

Carotid artery disease is not a niche problem. The US market for carotid intervention is substantial and growing, driven by an aging population, increasing awareness of stroke prevention, and a gradual shift from surgical to endovascular approaches.

The global carotid stent market is estimated at approximately $622 million today, growing toward $1 billion by the early 2030s at a CAGR of over 11%. The US represents the largest single market — and until June 2025, InspireMD had zero commercial presence there.

That changed with the FDA PMA approval.

But here’s what makes the opportunity even larger than those numbers suggest: the current approval covers symptomatic patients at high surgical risk. That’s a meaningful but limited population. The real prize — and the reason this story extends well beyond 2026 — is the potential expansion to standard surgical risk patients. That’s where carotid endarterectomy currently dominates with roughly 100,000 procedures per year in the US alone.

If CGuard Prime demonstrates non-inferiority or superiority to CEA in standard-risk patients — which upcoming trials are designed to evaluate — the addressable market doesn’t grow incrementally. It multiplies.

The long-term vision isn’t to be an alternative to surgery for patients who can’t tolerate it. The vision is to make endovascular stenting the first-line standard of care for carotid artery disease. Full stop.

The Commercial Launch: What The Numbers Show

InspireMD received FDA PMA approval in June 2025. Commercial launch began immediately, with the first US revenues reported in Q3 2025.

Here’s what the trajectory looks like:

- Q3 2025 (first quarter of US commercial sales):

- US Revenue: $497,000

- Total Revenue: $2.52M (+39% YoY)

- Gross Margin: 34.3%

- Q4 2025 (second quarter of US commercial sales):

- US Revenue: $866,000 (+74% sequential)

- Total Revenue: $3.1M (+62% YoY)

- Gross Margin: 37.5%

- US Gross Margin: ~70%

Two data points don’t make a trend. But 74% sequential growth in the second quarter of a commercial launch — while simultaneously growing international revenue 17% — is not nothing.

More importantly, the underlying operational metrics tell a story that revenue alone doesn’t capture:

- 500+ cumulative procedures completed since launch.

- 80+ centers have performed at least one case.

- 200+ centers in the pipeline at various stages of VAC approval and evaluation.

- 30+ person US commercial team in place, with roughly half having started only in Q4 2025.

That last point is critical. The sales representatives who joined in Q4 are still in the early stages of working through hospital Value Analysis Committees — the approval process that determines whether a new device can be used in a given institution. These processes take quarters, not months. The revenue contribution from half the commercial team is only beginning to materialize.

Management’s 2026 guidance reflects this: $13-15 million in total revenue, representing 45-65% growth over 2025. With anticipated acceleration in the second half driven by the expected TCAR indication approval and the introduction of an enhanced delivery system.

The Balance Sheet: Why This Company Has Time

One of the most important questions for any small-cap medtech company in launch mode is simple: do they have enough money to survive long enough for the strategy to work?

For InspireMD, the answer is yes, with an important asterisk.

As of December 31, 2025, the company held $54.2 million in cash, cash equivalents, and marketable securities. With a quarterly net loss of approximately $11.8 million, that represents roughly 4-5 quarters of runway at current burn rates.

That’s not unlimited time. But it’s enough time to reach several significant milestones that could fundamentally change the company’s capital position — including two remaining milestone-based tranches from the 2023 private placement, each providing $17.9 million in gross proceeds, tied to specific commercial and regulatory milestones expected in 2026 and 2027.

The company is not in a position where it needs to raise capital urgently at any price. That matters enormously when you’re evaluating the risk of dilution.

The Question The Market Is Asking Wrong

Most investors looking at NSPR see a small company burning through cash, with a stock price more than 40% below its 52-week high, in a competitive market dominated by large strategics with far greater resources.

That’s one way to look at it.

Another way: a company that just received FDA approval for a demonstrably superior product, is generating accelerating US revenue in only its second quarter of commercial sales, has a balance sheet that provides meaningful runway, and is building commercial infrastructure in the largest medical device market in the world — trading at a total enterprise value of approximately $60 million.

The market appears to be pricing in a difficult outcome. The operational data may be suggesting something more constructive.

Whether you find that disconnect interesting or irrelevant depends entirely on your time horizon and your conviction in the clinical evidence.

I find that disconnect interesting enough to keep following closely.

What I’m Watching. And What Could Change My Mind

This is the first article in a series on InspireMD. In the pieces that follow, I’ll go deeper on specific aspects of the thesis that I believe the market may be underweighting.

But the starting point is this: a company with best-in-class clinical data, a recently approved product, early commercial traction in the US market, and a balance sheet that gives it time to prove or disprove the story in public.

What would weaken my view? Slower-than-expected center activation, weak repeat usage, disappointing margin progression, or evidence that clinical enthusiasm is not translating into durable commercial adoption. Those are the signals I care about most from here.

I’m not here to give financial advice, but I am here to point out where the ‘machinery’ of the market is failing to see the obvious. Are we watching a trap, or the birth of a new standard of care? I’ve made my bet. Let’s see if the rest of the market catches up in next articles.

Next in the series: ‘What The Job Postings Told Me About InspireMD (NSPR)‘, the publicly available information that tells a story the stock price hasn’t figured out yet.

🟢 Disclosure: The author holds a position or has active interest in this name.

⚠️ I produce these analyses for my own enjoyment and because I’m always looking for new opportunities. I am not a financial professional, and I don’t have access to professional-grade tools or proprietary data. Everything here is built from publicly available information and my own reasoning — which means I can be wrong. This analysis may include forward-looking statements based on current expectations and projections; these are subject to risks and uncertainties that could cause actual results to differ materially from what is discussed here. I may not always see the full picture, and my views will change as new information emerges or as I come to understand data points I initially overlooked or underweighted. However, I am under no obligation to update or keep this information current as the situation evolves. I only operate with cash positions — no leverage, no margin, no shorting. I never bet against the market or individual companies. My analysis reflects the company’s fundamentals, not its price action. The company is not its price, and the price is not the company. I express my own opinions. I am not receiving compensation to share this. I have no business relationship with any company whose stock is mentioned in this article. Nothing here is financial advice. Do your own due diligence.